TL;DR

Checkout is where a big share of revenue quietly slips away. With cart abandonment around 70%, small issues in payment options, mobile UX, or authorization flow add up fast. A solid stack combines fast checkout UX, reliable payment rails, smart fraud controls, and clear visibility into where customers drop off.

Different models need different foundations: D2C brands should optimize for mobile speed and easy guest checkout; omnichannel retailers for consistent behaviour across online and stores; multi-country players for routing to the best processor in each market.

Evaluate vendors like an operator: coverage for your key methods, behaviour under peak load, impact on approval rates, and how easily you can run experiments. Then run a 4–6 week pilot, tracking conversion, approval rates, step-level drop-offs, mobile time-to-checkout, and support tickets. If the numbers move, scale that layer. If not, swap the component, not the whole stack.

Why Payments Became a Stack, Not a Step

Checkout is no longer a single page to collect money. It is a system of gateways, routing, subscriptions, fraud controls, and UX choices that determines whether conversion lives or dies, renewals fire, and customers come back.

A few years ago, most retailers and brands ran payments through a single gateway bundled with their e-commerce platform. That worked when transactions were simple: one-time purchases, primarily cards, mostly domestic. Today, the reality is far messier. Retailers juggle cards, UPI, wallets, BNPL, COD, and recurring billing. When these sit in disconnected tools, it leads to reconciliation gaps, fraud blind spots, and inconsistent conversion.

Payment complexity has surged across retail and D2C, driven by regional payment preferences, the rise of subscriptions, and ever increasing customer expectations of seamless experience. Yet most retail teams still treat it as a gateway procurement decision, not as a layered architecture.

What’s at stake is revenue recognition, subscription churn, fraud losses, and long-term flexibility. If payments fail, everything upstream (marketing, merchandising, CX) instantly loses its ROI. A small drop in success rate hits monthly revenue. Retailers and brands now face a real operational question: How do you build a payment stack that keeps conversion high and risk low, without increasing operational overhead?

With cart abandonment around 70%, small issues in payment options, mobile UX, or authorization flow add up fast. If your current setup can't tell you why mobile conversion drops 40% compared to desktop, or which payment methods drive the highest approval rates, you're leaking revenue at your most critical touchpoint.

The answer starts with understanding what's actually running beneath the checkout button.

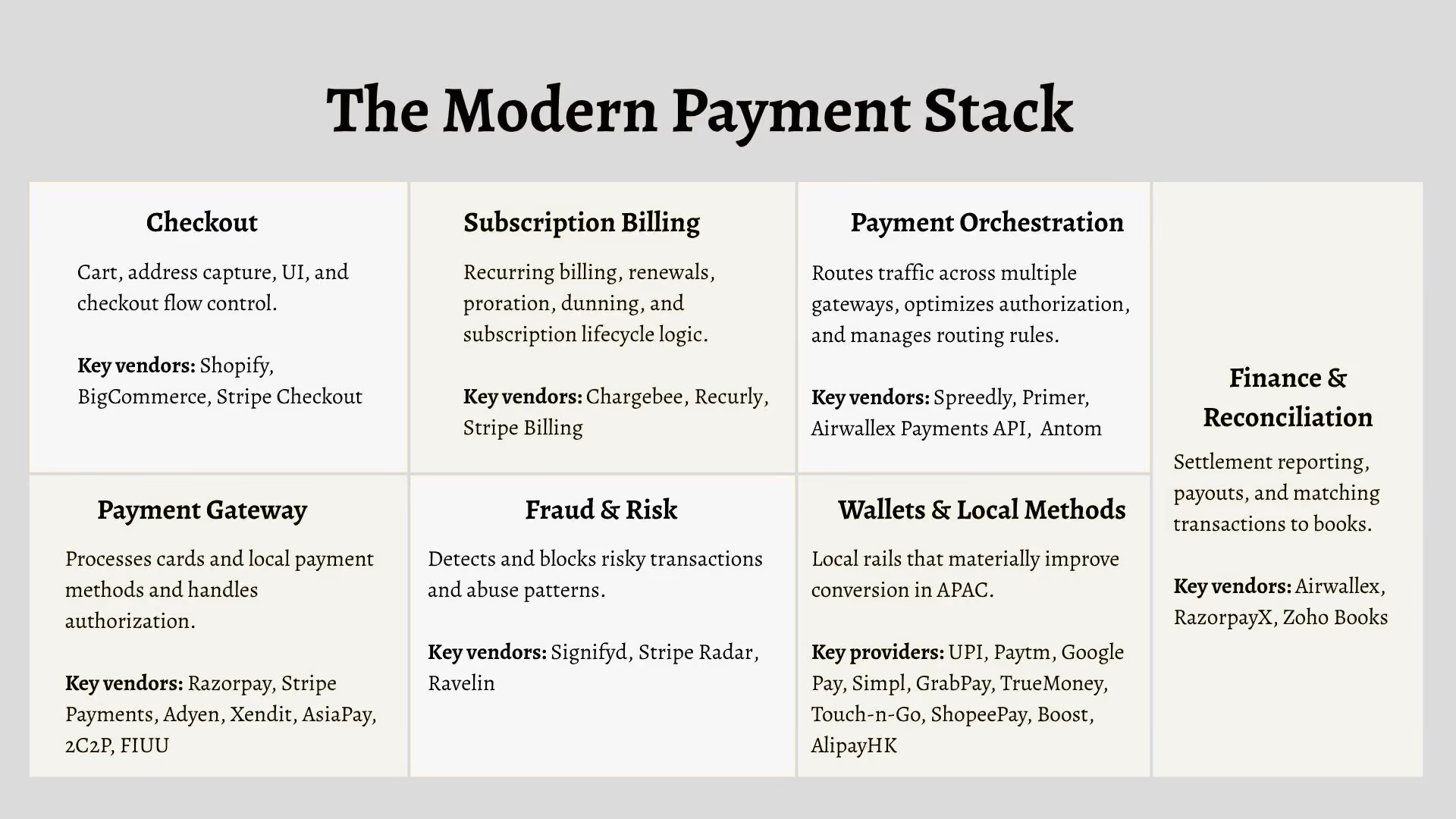

Core Building Blocks of the Payment Stack

A modern retail payment is a layered system that handles routing, renewals, fraud, wallets, and the UX that ties it all together. Here’s what most retailers and brands actually run beneath the surface:

Checkout Layer

- What it is: The touchpoint that decides whether a customer converts or abandons. It controls cart logic, address capture, shipping rules, validation, and the overall checkout UX.

- Dependencies: OMS, CMS, inventory accuracy.

- Vendors: Shopify Checkout, Bolt, BigCommerce

Payment Gateway

- What it is: The transaction rail that keeps money moving. It authorizes payments, handles card flows, routes to banks, and determines whether a transaction clears or fails.

- Dependencies: Bank accounts, KYC approval, settlement timelines.

- Vendors: Razorpay, Stripe, Adyen, PayPal, Xendit, AsiaPay, 2C2P, Fiuu

Subscription Billing

- What it is: The engine behind renewals and recurring revenue. It manages renewals, proration, dunning, retries, and subscription lifecycle events.

- Dependencies: Gateway tokens, CRM records, OMS events.

- Vendors: Chargebee, Recurly, Stripe Billing (some regional billing engines exist but global players dominate)

Fraud & Risk

- What it is: The guardrail that filters good customers from bad actors. It scores transactions, flags risky behavior, blocks fraudulent attempts, and reduces chargebacks.

- Dependencies: Gateway event feeds and real-time behavioral data.

- Vendors: Signifyd, Stripe Radar, Ravelin

Payment Orchestration

- What it is: The logic layer for merchants using multiple gateways. It routes transactions intelligently, optimizes success rates, and balances load across providers.

- Dependencies: Multiple active gateway contracts.

- Vendors: Spreedly, Primer, Airwallex Payments API, Antom

Wallets & Local Payment Methods

- What it is: The APAC essentials shaping conversion today. It supports UPI, mobile wallets, BNPL options, and COD—methods that dominate checkout preferences in many markets.

- Dependencies: Checkout layer, settlement cycles that differ from card rails.

- Vendors: UPI, Paytm, Google Pay, Simpl, GrabPay, TrueMoney, Touch-n-Go, ShopeePay, Boost, AlipayHK

Taken together, these layers form the spine of your revenue operations. What matters isn’t just choosing strong components, but ensuring they work as one system that keeps both conversion and cashflow predictable.

Three Typical Stack Approaches

Once retailers understand the layers, the next question is how to assemble them into a stack that fits their maturity, markets, and product model. Most mid-market brands gravitate toward one of three patterns that balance speed, control, and operational effort differently.

1. All-in-One Payment Platform

Formula: Checkout + Gateway + Risk (+ Billing Lite)

One provider handles checkout components, payment processing, basic subscriptions, and often risk tools in a single contract and dashboard.

Who it suits: Best for retailers that value speed to market over deep customization.

Why it helps: Unified reporting simplifies reconciliation for finance, and product teams have fewer integrations to maintain as channels grow.

Key vendors: Razorpay, Stripe, Adyen.

2. Modular Checkout + Gateway

Formula: Custom Checkout Layer + Gateway(s) + Risk + Wallets

A flexible checkout layer controls UX and cart logic, while one or more gateways handle processing and settlement in the background.

Who it suits: Better for brands that treat checkout as a growth lever and have an in-house product/engineering team or a SI partner.

Why it helps: You can experiment with layout, steps, address logic, and payment placement to squeeze more conversion out of the same traffic.

Key setup: Checkout.com or similar as the processor, plus a custom or highly configurable checkout layer.

3. Subscription Platform + Standard Gateway

Formula: Checkout + Standard Gateway + Chargebee/Recurly

A dedicated subscription platform owns renewals, proration, pause/skip, and dunning, while a standard gateway handles the actual charge.

Who it suits: Brands with memberships, autoship, replenishment, warranties, or mixed one-time and recurring carts.

Why it helps: You get cleaner subscription metrics, precise lifecycle control, and recovery workflows that reduce involuntary churn.

Key vendors: Chargebee + Stripe/Razorpay

The Trade-Offs: What You’re Really Balancing

1. Unified Suite vs Modular Flexibility

Unified platforms reduce integration and simplify reporting; modular stacks unlock deeper control, routing logic, and UX experimentation but add moving parts.

2. Checkout Speed vs Customization Depth

Native checkouts convert faster on mobile; custom checkouts allow differentiated journeys and layout tests but require ongoing engineering effort.

3. Subscription Sophistication vs Operational Load

Dedicated billing improves renewals, proration, and churn recovery, while increasing reconciliation work and the need to sync billing, orders, and payouts.

4. Authorization Uplift vs Routing Complexity

Multi-gateway routing lifts approval rates and provides redundancy, but comes with orchestration fees, extra contracts, and higher operational oversight.

5. Local Coverage vs Consistency & Control

UPI, wallets, BNPL, and COD boost APAC conversion, but complicate refunds, settlements, dispute handling, risk tuning and increase migration friction later.

Evaluation Framework: Score Each Vendor 1–5

Evaluating payment vendors is less about feature lists and more about how they behave under real retail conditions — peak traffic, mixed carts, failed renewals, and multi-market expansion. Score each vendor from 1 (basic) to 5 (advanced) across these eight dimensions:

1. Integration Effort

Assess: Native connectors to OMS, ERP, and ecommerce APIs; webhook quality.

How: Count native integrations, skim API docs, run a small pilot sync.

2. Checkout Flexibility

Assess: Ability to adjust flows without heavy dev work; mobile UX; one-click profiles; address validation.

How: Ask vendors to demonstrate a live flow change and review end-to-end mobile journeys.

3. Subscription Maturity

Assess: Renewals, pause/skip, metered billing, dunning, recovery workflows.

How: Walk through key subscription scenarios; check what’s handled by config vs custom code.

4. Authorization Performance

Assess: Smart routing, retry logic, risk scoring, uptime, latency under peak load.

How: Request performance metrics and uptime logs; understand regional routing rules.

5. Fraud & Risk Engine

Assess: Adaptive scoring, rule transparency, false-positive control.

How: Review rule configurations, sample decisions, and update frequency for new fraud patterns.

6. Total Cost of Ownership (3 Years)

Assess: Processing fees, add-ons, orchestration costs, implementation and ongoing ops effort.

How: Model three-year volumes; request detailed cost breakdowns.

7. Reporting & Reconciliation Quality

Assess: Structure of settlement exports and how cleanly they map to finance systems.

How: Review sample payout files with your finance team.

8. Exit Risk & Portability

Assess: Token portability, ease of exporting customers/subscriptions, contract flexibility.

How: Validate export formats and review terms on notice periods, penalties, and data retention.

Buyer’s Checklist

Here is a 10 point checklist that you can use to make your buying decisions.

- Implementation: Who owns implementation end-to-end, and what does cutover look like for a retailer our size?

- Operations: Which team runs day-to-day config, and what skills are required?

- CX Control: What customer-facing elements can we edit without engineering?

- Disputes: How are disputes and chargebacks handled, and what views do CX and finance get?

- Support: What is your incident support model, and how do escalations work?

- Regulation: How do you manage and roll out regulatory changes across our markets?

- Roadmap: What drives your next 12–18 months of product priorities?

- Enablement: What training will our teams receive pre- and post-go-live?

- Incidents: What were the most serious incidents last year, and what changed afterward?

- Expansion: What steps are required if we add brands, channels, or countries?

Final Guidance & Scenario Fit

Different retail models need different payment stacks, based on team maturity, channel mix, and the role payments play in revenue operations. Here’s how that plays out across a few scenarios:

- Fast-Growth D2C Brand (≤ 50 SKUs)

- Recommended Stack: Shopify Checkout → Stripe/Razorpay → Chargebee (if subscriptions grow) → Stripe Radar

- Why: Fast to launch, strong local payment coverage, and minimal engineering requirements. Ideal for brands focused on growth rather than custom flows.

- Watch-outs: Checkout customization is limited; upgrades often require workarounds.

- Omnichannel Retailer (10–200 stores)

- Recommended Stack: Adyen/Stripe gateway → Primer (orchestration) → Chargebee (subscriptions) → Signifyd (fraud detection)

- Why: Multi-gateway routing improves authorization rates across regions, and pairing it with strong fraud control and subscription logic keeps operations predictable as volume scales.

- Watch-outs: Orchestration adds complexity; ensure ownership of routing rules.

- Multi-country Retail Enterprise Operating Across APAC

- Recommended Stack: Adyen + Spreedly (orchestration) → Custom checkout → Recurly/Chargebee → Ravelin

- Why: Supports complex routing, regional payment preferences, multi-entity billing, and the custom checkout design required for market-specific UX.

- Watch-outs: Engineering-heavy; prioritize maintainability.

A payment stack is an operational backbone rather than just a gateway decision. Start with reliability and clean reporting. Add subscription logic only when the model is mature. Optimize checkout UX continuously.

Next steps

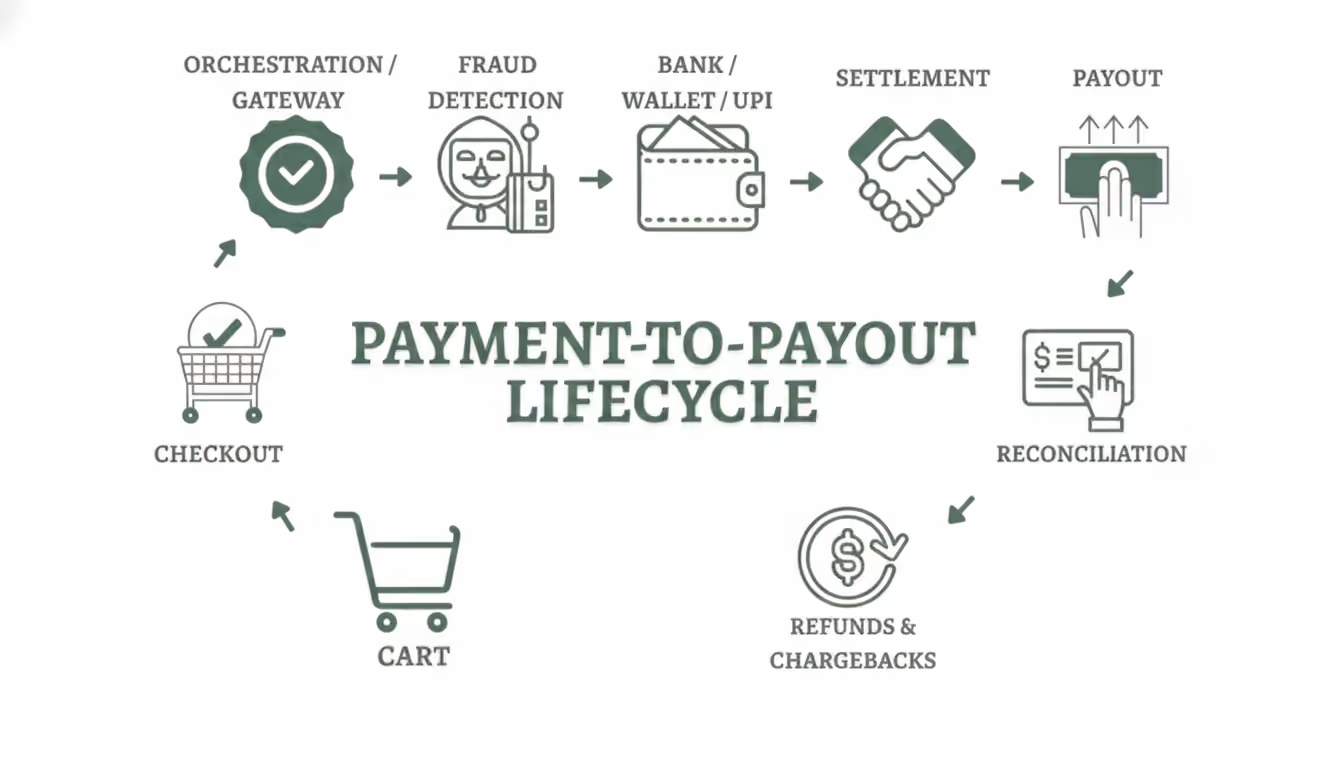

- Map your current payment-to-payout flow to identify gaps in checkout, routing, subscriptions, and finance reconciliation.

- Shortlist vendors based on your stack philosophy and the payment methods that genuinely influence conversion.

- Run a 4-6 week pilot on real traffic to validate authorization rates, mobile checkout performance, and subscription handling.

- Align finance, CX, and product early so migration, refunds, and disputes don’t become blockers at go-live.

Build for authorization stability first. Experimentation comes next.

Your payment stack is where revenue either clears or rolls back, so treat every decision like an operator making a long-term infrastructure call.

.avif)

.avif)